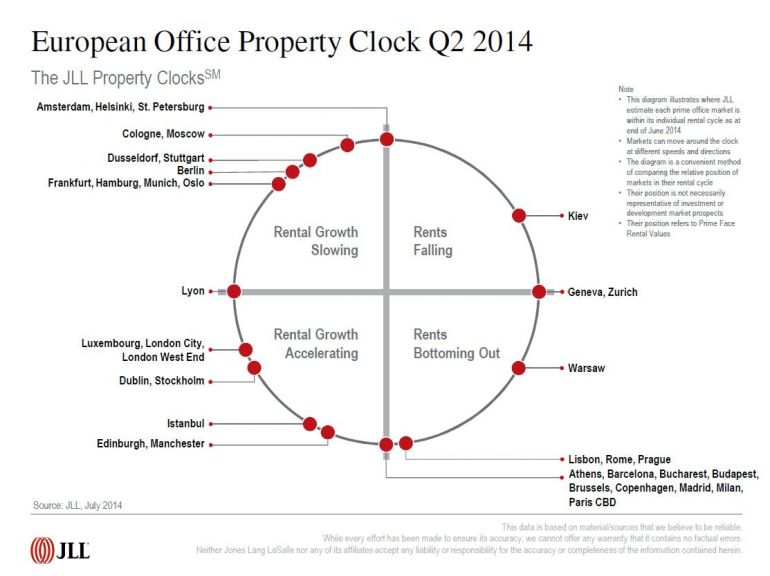

Developed by JLL report "European Office Clock" using the clock diagram compares the relative position of the markets in Europe in the next phases of the cycle changes the most attractive lease rates for office space. This scheme takes into account four phases: accelerating the growth of rental rates, slowing growth in rental rates, accelerated decline in occupancy rates and rents falling to a minimum.

The increase in rental rates

ILL The report shows that compared to the previous three months, the cost of the lease on the office market in 24 European countries rose by 0.4 percent, which experienced particularly cities such as Dublin (by 7.1 percent), Munich (3.2 percent) and Madrid (1 percent). Due to the high level of new supply declines reported in Prague (by 2.5 percent), while in other markets, rents have remained stable.

Due to limited availability of high quality office space, rents in the European market is likely to grow. Rental rates for office space in Warsaw at the end of the second quarter. 2014 years remained stable and ranged between 22 and 24 euros per sqm. of month in the center of Warsaw and from 14.50 - 14.75 in the most popular locations outside e.g. in Mokotow. Rents for the most prestigious office buildings in Warsaw are the highest in Central - Eastern Europe. However, it should be noted, that the high new supply entering the market would be reflected in an increase in vacancy rates, which in turn will result in further downward pressure on rental rates. I think that Warsaw will remain in the zone between the hours of 3 and 6 in the statement of Office Property Clock to the end of 2016 - says Mateusz Polkowski, Director of the Department of Research and Consulting JLL.

There is a growing activity of tenants

In the last quarter has revived the European market for office space lease. Tenants total of 2.8 million sqm., Which is about 19 percent more than the previous quarter and 11 percent more than the same time last year. Moreover, ILL report that the second quarter of 2014 years in terms of office space rental was the best since the last quarter of 2012. The increase in Western European markets proved to be possible, thanks to the high activity of tenants - in Paris, London, Stockholm, and in Brussels, Milan, Lyon. Among the countries of Central and Western best results were recorded in Warsaw and Budapest.

JLL argues that the demand for offices in Europe in 2014 will grow by 6 percent in 2015 and by a further 5 percent.

From the point of view of the developer

The winning streak was also accompanied by the developers - a European office resources increased by 1.3 million sqm., An increase of 33 percent more than the first quarter, while the supply of offices has increased by 76 percent compared to the same period last year. The best results noted in Moscow and London.

ILL Data show that the supply of office space in the European market will continue to grow. 2014 will be another year under the sign of a very large development activity in Warsaw. Today the total office stock in Warsaw are 4.3 million sqm. and another 579 000 square meters. is in progress. It is also worth mentioning the 62 000 sqm. to retrofit older office projects. Our analyzes show that in 2014 the Warsaw office market can enrich by up to 350 000 sqm., which will be even better than the 300 000 sq m. recorded in the previous year. At the same time, it should be noted, that Warsaw is still popular among tenants, even though demand eased somewhat this year compared to previous years. We believe this is mainly due to the very low number of transactions in 2009, which is now, or after 5 years reappear on the market. From our analysis, however, shows that the second half will bring several large rental contracts - says Tomasz Czuba, Director of Office Leasing JLL in Poland.

The vacancy rate

The decline in leased office space noted in the middle of the countries surveyed. In particular, it relates to Edinburgh, Budapest, Amsterdam and Dublin. The indicator remained stable in Moscow, in turn, has increased in London. JLL analysts argue that with the increase in the activity of tenants, the vacancy rate will slowly decrease.

Download PDF